Cash Flow Planning into Retirement

Learn about the term “sequence of returns” and its overall impact in retirement.

One of the most important conversations we have with clients nearing retirement is about ensuring they have adequate access to cash or cash-like investments as they transition from earning a paycheck to drawing down their investment assets.

A well-known example that illustrates the importance of this strategy is the Global Financial Crisis of 2008. Imagine someone who retired in October of that year. In just the first six months of their retirement, the S&P 500 dropped by more than 25%. If that retiree didn’t have enough cash set aside, or if their portfolio wasn’t properly diversified, they may have been forced to sell investments at a significant loss just to cover everyday expenses.

Selling during a market downturn not only locks in potential losses but can also significantly hamper a portfolio’s ability to recover when markets rebound. This phenomenon, known as sequence-of-returns risk, can shorten the longevity of a retirement portfolio, especially if large losses occur early on.

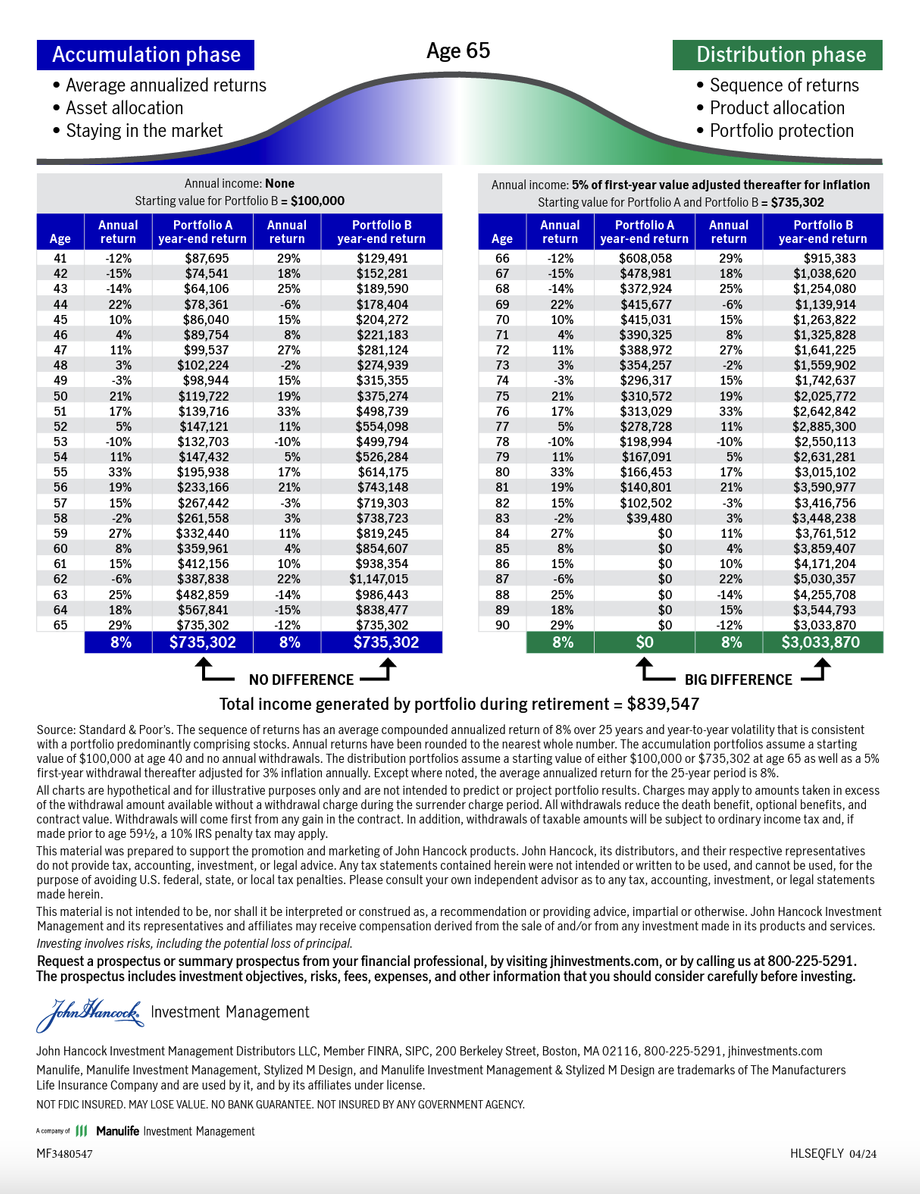

Below is a chart that shows the difference in portfolio values during the Accumulation and Decumulation phase of Investing. In reference to the Distribution phase on the right, while the average return is the same as in the Accumulation phase, the difference in ending portfolio values is drastic due to when the returns occurred, either in the early stages or later stages of retirement.

Key Steps to Take Before You Retire

To help avoid this situation, here are two essential strategies we typically recommend:

- Maintain an Emergency Cash Reserve: Aim to keep six to nine months' worth of expenses in readily accessible cash. This gives you flexibility and peace of mind without having to sell investments in volatile markets.

- Build a Diversified, Non-Correlated Portfolio: Diversification reduces risk by spreading your investments across asset classes that don’t move in lockstep. A well-balanced portfolio can help soften the impact of market downturns and improve overall stability.

Retirement is a major life transition; we believe thoughtful cash flow planning can make all the difference in protecting your financial future. If you're nearing retirement and haven't yet addressed your short-term cash needs or reviewed your portfolio’s diversification, now is the time to do so.

The information provided is for informational purposes only and not intended to provide investment, tax, or legal advice. Neither the information provided, nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. All investing involves risk including possible loss of principal. Any investment strategies that are presented may not be suitable for all investors. Information contained herein has been obtained from sources considered to be reliable, but we do not guarantee their accuracy or completeness. Steward Partners, its affiliates, and its Wealth Managers, do not offer tax advice. We suggest discussing your specific situation with a financial and tax professional before making any decisions. Past performance is no guarantee of future results.

Diversification does not assure a profit or protect against loss in a declining market.

AdTrax 8582362.1 Exp 11/27